Commercial Rollout of LED Downlighters

The major stumbling block in 2009 and 2010 was that LED lamps were still in their infancy from a technology perspective. There was therefore significant skepticism around the following areas:

- Ability to match the lumen output of the light source that it was replacing

- Since the technology was so new and the lifetime of the lamps were being touted as 50 000 to 100 000 hours nobody could with any certainty verify this as all the lifetimes were being measured with different accelerated aging mechanisms and there was no standard that was agreed at that stage BUT everybody was selling the ROI based on these unproven lifetimes. To further add doubt to this – there were some cases where early adopters had their fingers burned by paying large capex amounts only to find that the technology failed prematurely and that there was no warranty to back up these life claims.

Karebo at that stage had just completed rolling out more than 40 million CFL lamps into households for Eskom since 2004 and realized that this wave was coming to an end.

We had scanned the market looking for what would be the next wave to CFLs and realized it was the LED lamp. Due to our close working relationship with Philips Lighting we had access to their Research and Technology pipeline.

In mid 2009 we found a LED lamp that we tested that ticked the following key boxes

- Produced a similar lumen output to an existing halogen lamp – it was not an one to one match but was within the 80th percentile mark to make a case for a retrofit

- The price on volumes – with co-funding from either Eskom or carbon funding – created a financial model that could over the price barrier to entry.

We played around with models but one of the key stumbling blocks was the form factor of the lamp. The lamp we settled on was a long form lamp that operated at 230 V and we planned to do a changeover from 12 V to 230 V and priced in a R 40 per lamp installation cost based on market prices we received from contractors in the market. In fact the installation rates we received were higher than R 40 per lamp but we capped it at R 40 believing that based on volumes we would be able to secure these services when required. When we did eventually roll out the project – using internal installation teams we found that this cost was excessively inflated. We managed to half this and to still be profitable. We were trying to get the first mover advantage by ensuring that cost barriers could be removed whilst still ensuring that the project remained profitable and delivered significant savings. We needed it to be a win/win for all involved.

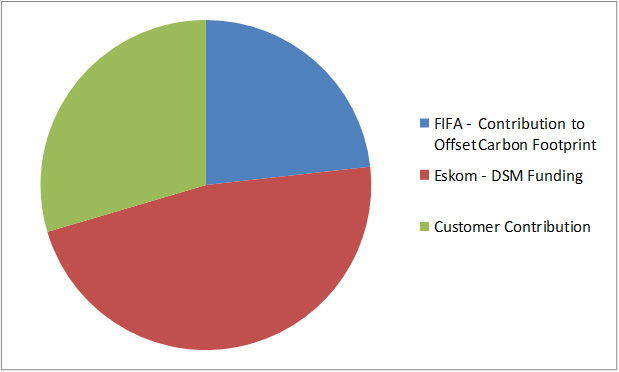

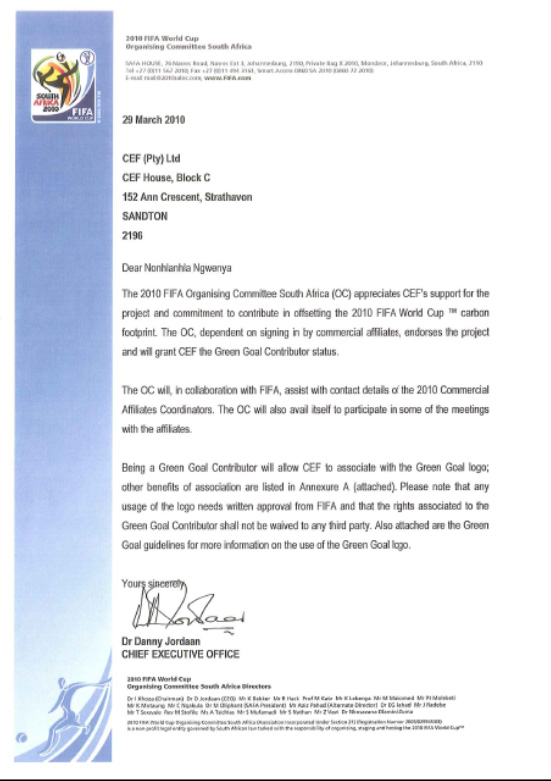

We spent several months exploring a carbon funding option with CEF and arrived at a scheme where we could use the FIFA 2010 World Cup to market the following financial model:

We submitted a very detailed presentation and after a long process received approval in March 2010 to rollout the project – see below from FIFA:

The approval came 3 months too late. The plan was to rollout the project prior to the World Cup and obtain the publicity associated with it. We initially expected to get approval in December 2009 and to be complete by May 2010.

We stopped the process after this and picked it up again after the World Cup. At that stage 15 months had passed since we had first started exploring this project. In that time the prices of the lamp were falling and in mid October we managed to reach a price point where we could roll the lamps out with only Eskom funding and a minimal contribution from the customer.

The second advantageous thing to happen was that we received a new 12 V lamp from Philips that had the same form factor of the old halogen lamp and therefore we could do simple retrofits and contain the installation costs.

By not outsourcing any of the installations we also managed to contain the installation costs to a manageable point to make the project financially viable. The omission of the carbon aspect was also a bonus as there are additional hurdles to overcome with that funding mechanism.

The other vital contribution to the success factor was that we managed to convince Philips to give us a 3 year warranty on the lamp to remove the skepticism around the lamp life. This key concession from the leading lighting brand paved the way for this warranty to now become the norm in the industry. We submitted a proposal to Eskom for funding in November 2010 and received approval in March 2011.

In June 2011 we went to market with the following offer – the customer contributed R 60 per lamp – costs included lamp and installation – and got a high quality 12 V LED lamp. If the customer wanted to do the conversion from 12 V to 230 V we added a further R 12 for additional labour charges. The typical payback for our customers was between 4 and 8 months. The project was a roaring success.

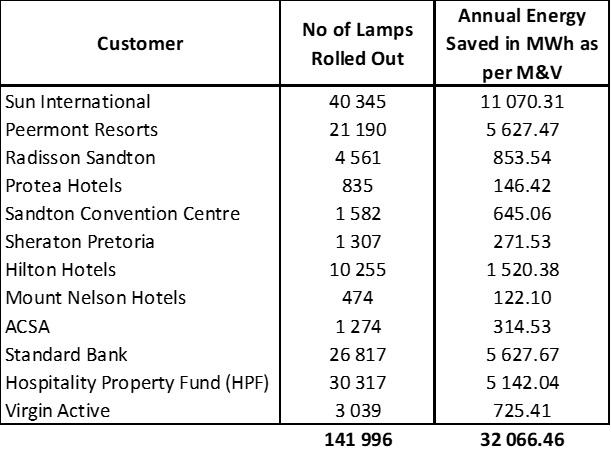

The original intention was to rollout 200 000 lamps to achieve a 36 GWH annual reduction with a 4 MW peak load reduction. We managed to achieve a similar output with only 142 000 lamps.

This demonstrated that our energy models were conservative but sound and that the financial model also worked. The customers that participated in the initial phase and were the trail blazers were:

1 How the Project Makes a Contribution to Energy Efficiency and Renewable Energy

- This project created a lot of interest in the market and led to the development of the standard offer model for LEDs only at 55 c per kWh.

- The 3 year warranty has become the industry norm

- Karebo made its own contribution to the measurement model by using an energy derived saving converted to a Rand per MW model

- Halogen downlighters are used quite significantly in the hospitality sector and the residential sector and this first project paved the way for a financial and energy model to allow this inefficient technology to be removed – thereby contributing significantly to a reduced Eskom evening peak by greater adoption of this retrofit with Eskom funding.

- LED downlighters are also now being rollout out in the residential sector after the successful completion of this project

2 List of the Past and Future Actions, deliverables and Milestones of this Project

- This project subsequently led to a second LED rollout phase that Karebo rolled out to:

- Tsogo Sun Properties

- ABSA

- Growthpoint Properties

- The second rollout was done with no customer contribution as the lamp costs had reduced further – this was not a downside to any of the customers from phase 1 as this was done 12 months later and the paybacks from phase 1 was between 4 and 8 months per customer in phase 1.

There is now a fair comfort level with LED downlighters technology to the extent that they are being rolled out in the residential sector as well with some similarities from this project. These similarities are:

- 3 year warranty

- Fixed price to make it a free offer

3 Karebo Summary

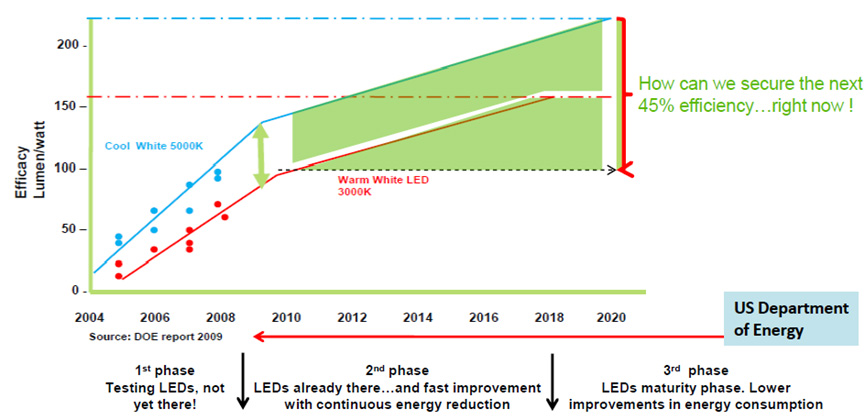

There were significant barriers to entry for this technology that would have been removed at some point in time. Karebo would like to believe that we moved this timeline up to a few years earlier. Our belief is borne from a US DOE study that looked at LED development in relation to time (there is also a correlation to price in this) – see below

A mid point in the curve is 2014 to 2015. To date Eskom has funded a substantial amount of LED downlighters long before this time and we would like to believe we played some part in that.

PROJECT IN ONE SENTENCE

The very first rollout of LED downlighters funded by Eskom IDM.

LEDs as a potential efficient light source were being touted as the next best thing in the late 2000s. The major barrier to entry to the technology into the market place then was cost.

The key selling points of LEDs were and still are:

Substantially reduced energy consumption

Substantially longer life times than the conventional lamps it replaces